Downgrades

Late Friday, Standard & Poor’s Ratings Services announced cuts on 9 euro zone member countries. It downgraded France and Austria by one notch (from AAA to AA+) but retained the AAA rating on Germany. See Chart 1 for complete rating changes (source: Standard & Poor’s Rating Services).These new ratings not only better align with risk premia already observed in financial markets but also create structural incentive for euro-zone members to work together with a greater sense of urgency and coordination to address the sovereign debt issue. Net-net, Germany is likely to benefit.

News of downgrades was leaked to financial media early Friday. Market resilience, especially a strong rebound from the day’s lows in U.S. stocks, added fuel to the U.S.- Europe decoupling talk, which has been buoyed by the recent stock market upswing and macro data releases.

The U.S.-Europe decoupling thesis is likely rational exuberance since monetary policies, economies and political interests have remained very much intertwined, if not more so now than before. The recent upswing in stock markets (in U.S. and Europe), reduction in risk premia (in European bonds and SP500 VIX (chart 2), etc), and the muted reaction to alerts of imminent downgrades Friday are likely indications of risk being priced out rather than in.

QE 3

Speculations about additional quantitative easing by the Fed are getting intense - see Fed to Weigh Further Easing Amid Doubts about Recovery (1/13/12) from CNBC.We discussed prospects of QE3 in Hope and Resistance (11/11/2011). We concluded that if history is a guide and also from a technical analysis and Elliott wave perspective, odds favor at least one if not two more rounds of policy accommodation (most likely QE in this case). Please see details in that piece.

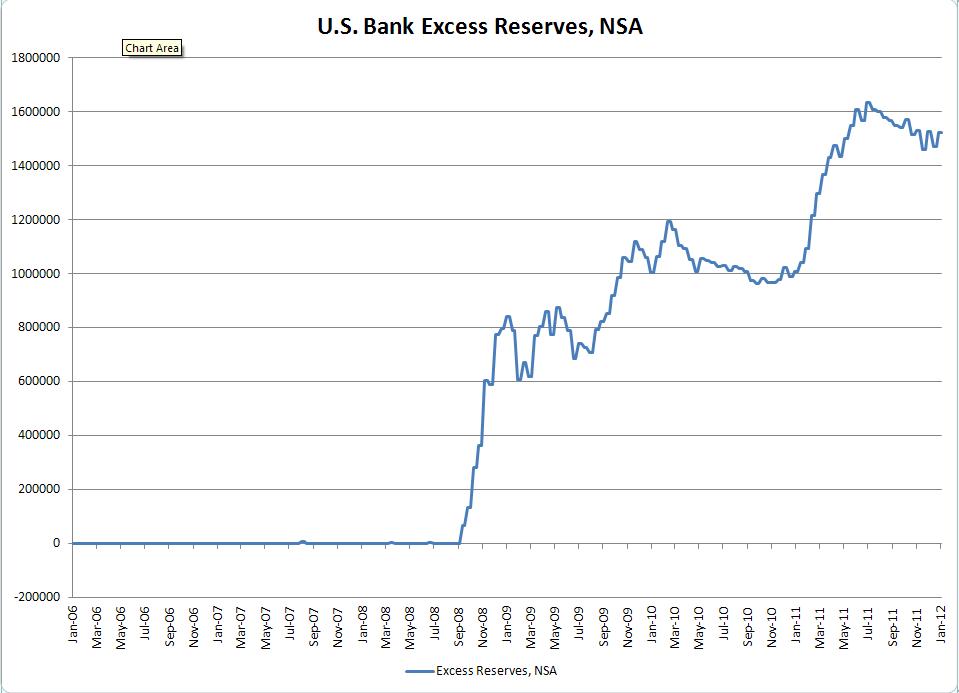

We showed Chart 3 on U.S. bank excess reserves then with full annotation. Chart 4 updates, with the most recent data without annotation. Our conclusion remains unchanged - the stage is potentially set for another round of (quantitative) easing.

Top tick

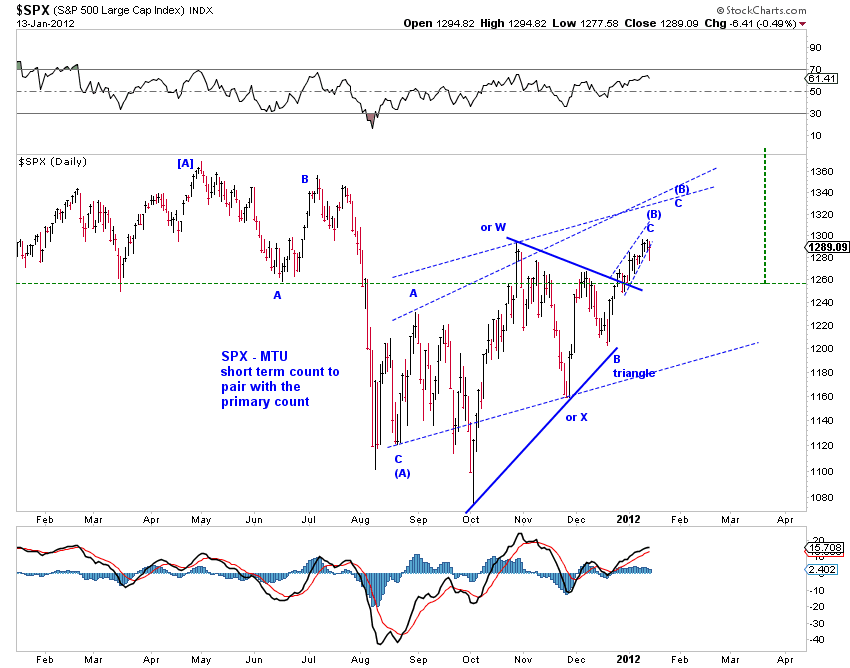

A logical place for a top tick in U.S. stocks could be in place from a wave structure perspective based on the primary count (Chart 5). (Please see recent weekly commentaries for top alternative counts.) In addition, Friday morning's decline in SPX broke a key support trend line which is now potential resistance.

It's possible to count a complete zigzag from the December low in SPX (Chart 6, blue). Under this interpretation, the rebound from Friday's low is a small degree wave ii which "kisses" the prior support line (red, Chart 6) and is likely to say "goodbye". A key risk to this generally bearish interpretation is additional quantitative easing (see above), but market can move faster than the Fed.

The near term bullish alternative sees the top tick after a small-degree wave [v]-up run. But it's now prudent not to take it as a given. One higher high at a time.