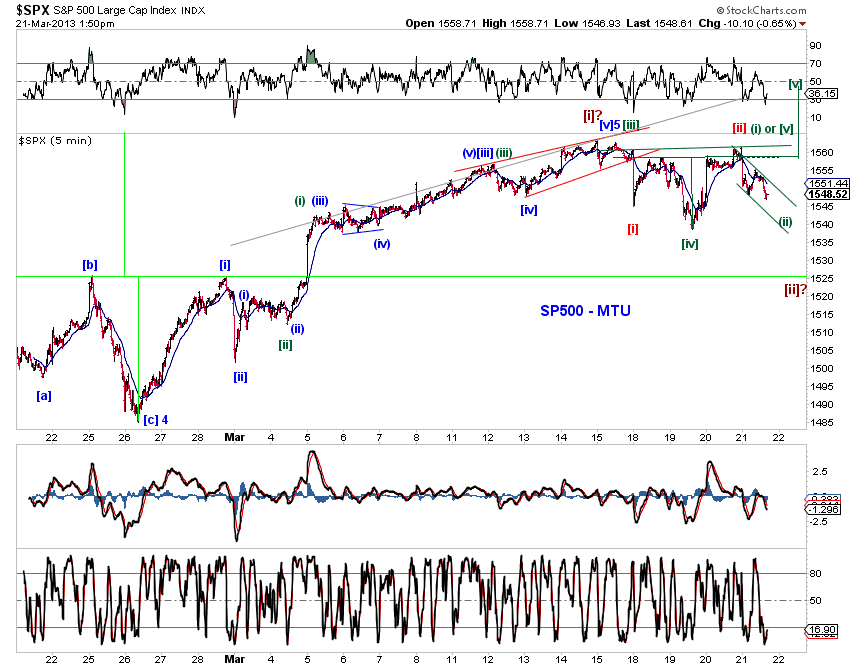

The upswing since the November 2012 low is likely approaching its end (Chart 1, blue). The top near term bullish alternative would be a small-degree 3rd wave extension (Chart 1, green) or 5th wave extension (Chart 1, red) which at this point is far from certain.

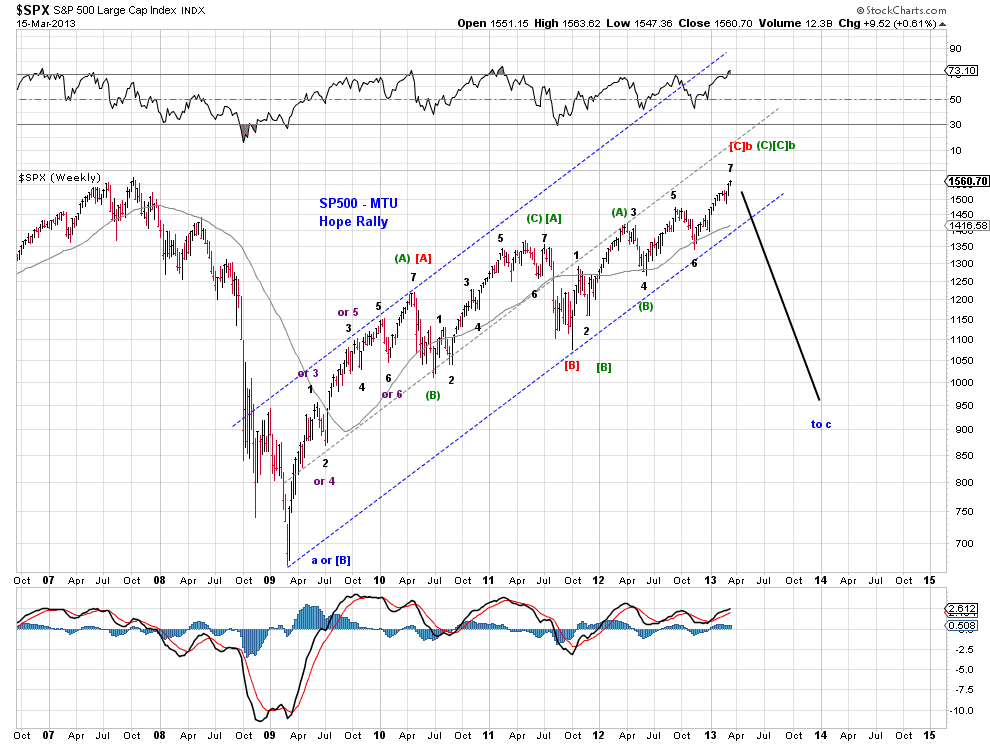

From a long term perspective, the pending top has the potential to complete the upswings at several degrees, potentially the Hope Rally itself. The best bullish alternative scenario since the 2009 bottom is an ending diagonal triangle (Chart 2). See A View from a Top (3/15/13) for details.

Bonds -

Treasuries sold off in early March but recovered all their losses by the end of the Month (Chart 3). The profile of the upswing in 10Y yields since their multi-decade-low in 2012 remains corrective and well contained by a base channel. Until bond yields breakout, the potential for one more rally (Chart 4) deserves proper consideration.

USD -

The USD index is attempting to breakout to the upside (Chart 5), but upside momentum is waning and bearish divergence has surfaced (Chart 6). A near term retrace (Chart 6, blue) or an outright reversal (Chart 6, red) is not out of the question.

The proposed range-bound profile for USD continues to track. Larger degree tracking counts for the 70-90 range in Chart 5 are still on the table.

Gold -

The proposed wave [4] correction in Gold (priced in USD) continues to track. Gold prices have attempted to defend their 2012 trend line support over the past month (Chart 7).

Prices remain just above the near term "line in the sand." A decisive breach of current support level would suggest a measured target around $1300, which is well within the normal range of wave [4] and also represents a Fib-382 retrace of the prior wave [3] advance (Chart 8).

The proposed wave [4] has now reached parity with wave [2] in time (Chart 8), which is potentially bullish. However, a still shallow retrace and the potential for wave [4] to consume more time based on the tendency for alternation continue to suggest patience and caution when one attempts to capture the pending wave [5]-up.